Geopolitical developments in the Middle East have once again brought global aviation into focus. As tensions escalate across key oil-producing regions, the aviation industry is experiencing a ripple effect—most notably in fuel pricing, operational costs, and route planning.

For aviation operators, asset managers, and leasing platforms, these developments are not temporary disruptions but indicators of a volatile operating environment, which appears to be becoming the norm rather than an exception.

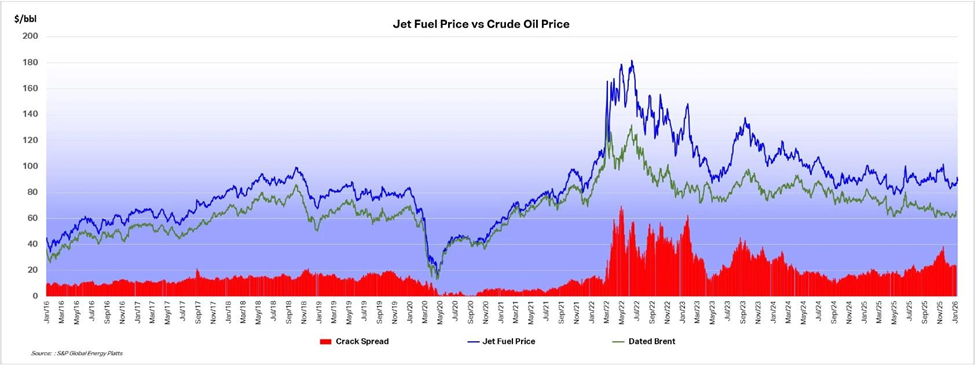

Rising Fuel Prices: A Direct Impact

The Middle East plays a critical role in global energy supply. Any disruption—whether logistical or geopolitical—has an immediate impact on fuel markets.

In recent weeks, instability in key transit routes such as the Strait of Hormuz has driven sharp increases in crude oil prices. As a result, jet fuel costs have surged, placing pressure on airlines and charter operators worldwide.

Fuel typically accounts for up to 30–40% of an airline’s operating expenses, making it one of the most sensitive cost components. Even a modest increase in fuel prices can significantly affect profitability and pricing strategies.

Increased Cost Pressure on Airlines

As fuel prices rise, airlines are compelled to adjust their pricing structures and operational strategies.

Many carriers have begun introducing fuel surcharges or increasing ticket prices to offset rising costs. At the same time, airlines are reassessing capacity, optimizing load factors, and focusing on cost-efficient operations.

This environment is accelerating the need for flexible fleet strategies, where operators can scale capacity without long-term capital commitments.

Airspace Disruptions and Route Changes

Beyond fuel prices, the conflict is also affecting how aircraft move across regions.

Airspace restrictions in parts of the Middle East have forced airlines to reroute flights, particularly between Europe and Asia. These detours result in:

- Longer flight durations

- Increased fuel consumption

- Higher crew and operational costs

Over time, these inefficiencies reduce aircraft utilisation, manpower optimization and breed scheduling chaos and impact overall network planning.

Shifting Travel Demand

Uncertainty in the region is also influencing passenger behavior.

Travel demand to and through affected regions has softened, while other markets are experiencing shifts in traffic patterns. Passengers are becoming more price-sensitive and cautious, leading to shorter booking windows and fluctuating demand.

While global aviation demand remains resilient, the distribution of that demand is becoming increasingly uneven.

Fuel Supply and Availability Risks

In addition to pricing pressures, concerns around fuel availability are emerging in certain regions.

Supply chain disruptions have led to tighter fuel inventories in parts of Europe and Asia. This creates a dual challenge for airlines—managing both the cost and availability of fuel.

In extreme cases, prolonged disruption could lead to capacity reductions or schedule adjustments.

What This Means for the Aviation Ecosystem

The current situation highlights a broader shift in aviation dynamics:

- Volatility is becoming a constant, not an exception

- Operational flexibility is now a strategic necessity

- Cost efficiency is central to sustainability

For operators, this means focusing on fuel-efficient aircraft, optimized routes, and adaptable fleet structures. For leasing and asset platforms like Skypulse, it reinforces the importance of enabling scalable, capital-efficient aviation solutions that allow operators to respond quickly to changing conditions. Skypulse is continuously engaging its clients and partners and assisting them in developing flexible operational models that take into account supply chain squeeze, fuel price and availability volatility, regulatory and geopolitical uncertainty, shifting demand and customer behaviour patterns to ensure business continuity while minimising impact on cashflow and bottomlines.